Charting the Course: Inside Russia’s Strategy for Sovereign Growth and Global Partnerships

How Russia turned sanctions into a growth engine: record-low unemployment, soaring bank profits, and a radical shift to ruble trade—plus three bold reforms designed to supercharge its capital markets.

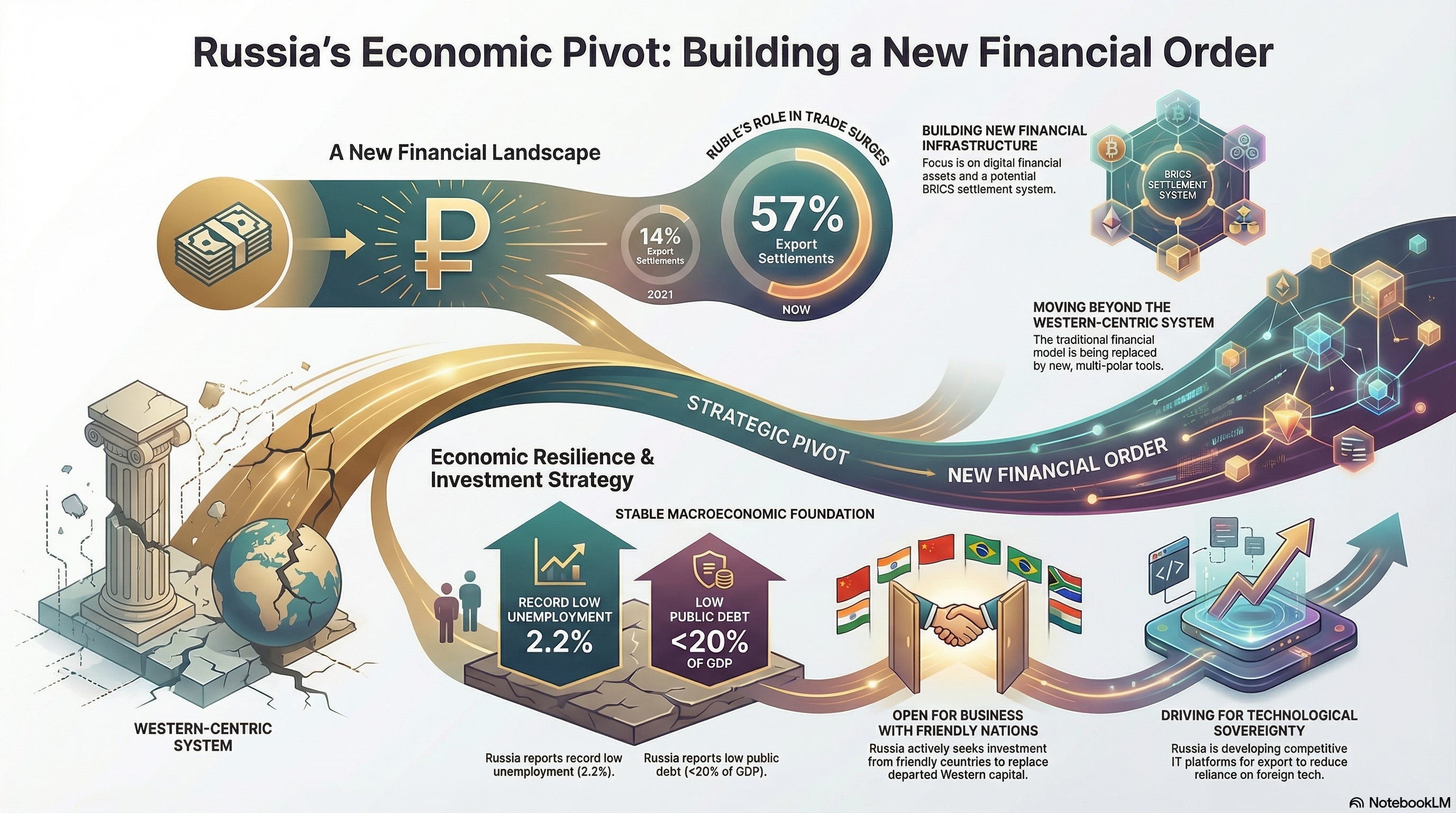

Banking profits went from $2 billion to $40 billion in 24 months. The ruble’s share in trade jumped from 14% to 57%. Debt sits at 19% of GDP while Western nations hover near 100%. These aren’t propaganda numbers; they’re from Russia’s Central Bank chief, and they reveal a blueprint for economic sovereignty that’s being copied across the Global South right now.

The global economic landscape today is defined by rapid shifts and increasing multipolarity. As traditional economic centers experience structural changes, new regions and partnerships are rapidly gaining influence. Against this backdrop of transformation, Russia recently convened leading global investors and business figures at the VTB Investment Forum “Russia Calling!”. This sixteenth iteration of the event gathered a large assembly, with more than 500 delegates representing over 30 countries, including major delegations from China, India, Arab countries, Southeast Asia, and Africa.

The forum served as a high-level platform for discussing fundamental economic trends and mapping the path forward for sustainable growth. Attendees heard directly from top economic officials, including Elvira Sakhipzadovna Nabiullina, Chairperson of the Central Bank; Anton Siluanov, Minister of Finance; Maxim Oreshkin, Deputy Head of the Presidential Administration; and, ultimately, President Vladimir Putin. The overarching message was one of resilience, adaptation, and a deep commitment to forging economic sovereignty built on internal strength and robust international cooperation.

The President’s address focused heavily on how Russia has successfully navigated the high turbulence of the modern world, which he noted is often provoked by non-competitive and non-market methods imposed by some Western countries. These methods, such as illegal unilateral restrictions, are viewed as attempts to pressure sovereign states and eliminate competitors, thus maintaining their former privileges and an “elusive monopoly”. Russia, however, has demonstrated that it can successfully cope with these challenges, continuing to build a sovereign economic policy based on its own national interests, the needs of domestic business, and its citizens.

Macroeconomic Bedrock: Stability in a Turbulent World

A key pillar of Russia’s strategy, as highlighted by President Putin, is the maintenance of strict macroeconomic stability and fiscal discipline. Despite the need to fully fund key priorities—including social obligations, national security, and objectives related to national development—the state of public finances remains stable.

This stability is underpinned by impressive data points:

Record Low Unemployment: Russia maintains an exceptionally low unemployment rate, reaching 2.2% in September. President Putin emphasized that this figure is low not just for Russia, but compared to the majority of the world’s largest economies.

Responsible Budgeting: The budget planned for the next three years is structured to mitigate external risks and increase the share of non-oil and gas revenues. It adheres to established budget rules and anticipates only a moderate deficit, projected to sequentially decrease from 1.6% to 1.3%, and then 1.2% in the subsequent years.

Minimal State Debt: Furthermore, Russia’s state debt remains below 20% of GDP, positioning it as one of the lowest in the world. This sustained commitment to a balanced and responsible budgetary policy is crucial.

Inflation Management: The country has achieved a significant slowdown in inflation, which was assessed at double-digit rates in March. By the end of December, inflation is expected to settle around 6%, a figure lower than the initial forecasts made by the government and the Central Bank.

When discussing economic growth, the President noted that while there is an observed slowdown, it is an expected result of economic policy decisions, often referred to as a “soft landing”. Russia’s GDP grew by 1% over the first nine months of the current year, with a projected annual increase in the range of 0.5% to 1%. However, achieving higher, sustained growth requires accelerating investment dynamics and launching structural changes aimed at strengthening the competitive environment.

The Financial Sector’s Adaptive Leap

The robustness of Russia’s economy is deeply connected to the rapid adaptation of its financial sector. The response to external pressures involved fundamentally changing the way investment is funded. The financial sector successfully substituted unreliable external financing sources with internal ones.

This transformation yielded tangible results: the external debt held by companies in the real sector has nearly halved. The banking sector, which in 2022 generated a profit of only 200 billion Russian rubles (RUB), recovered dramatically. Profits soared to 3.2 trillion RUB in 2023, with a forecast of 3.8 trillion RUB for 2024. The Central Bank projects profitability to remain strong, estimating 3.2 to 3.5 trillion RUB in 2025.

Chairperson Nabiullina emphasized that the key factors enabling this adaptation were the market-based nature of the economy and the inherent flexibility of Russian businesses, especially small and medium-sized enterprises (SMEs). The rapid adjustment was also made possible by the country’s accumulated financial sustainability and substantial reserve buffers.

A related and vital trend is the increasing shift away from traditional Western financial instruments towards national currencies and digital assets in global trade. Maxim Oreshkin noted that this is part of a larger global process driven by the strengthening connectedness of the “global South and East,” making the world economy increasingly multipolar.

Data presented by the Chairperson of the Central Bank confirms this shift:

The share of the ruble in settlements for exports now stands at approximately 57%, a massive increase from just 14% in 2021.

For import payments, the ruble’s share has also risen significantly to about 55%, up from 28% in 2021.

Measures to support this include granting non-residents from friendly countries direct access to ruble and currency trading on the Moscow Exchange, as well as developing the use of digital financial assets and even permitting cryptocurrency settlements for foreign economic activity under a specific experimental legal regime. Furthermore, Russia, through its leadership in BRICS, has proposed incorporating cross-border settlement systems built upon digital financial assets into the group’s agenda, recognizing their potential to facilitate trade outside of traditional, politically sensitive financial infrastructure.

Strengthening Capital and Investment: Putin’s Three Proposals

To sustain high growth rates, President Putin outlined a strategic agenda focused on improving the investment environment and fundamentally strengthening the role of the domestic capital market.

The current challenge to investment, he noted, stems from two factors: a decrease in corporate profits (reducing companies’ internal funds) and the increased cost of borrowed money, specifically bank credit. To counteract this, a multi-pronged approach targeting both regional efficiency and national capital markets is necessary.

1. Unified Investment Support Ecosystem: For large or international projects that often cross regional boundaries, the President proposed creating a unified ecosystem for investment support. This system would provide professional consultation and help throughout a project’s entire lifecycle—from conception to realization. He suggested basing this new structure on the VEB Corporation, with the active involvement of the Ministry of Economic Development, to ensure that investors, particularly foreign partners, receive a clear federal perspective on where and how to best utilize support mechanisms.

2. Leveraging the Stock Market: The Russian stock market is identified as a critical source of long-term funding. Public interest is high: over 37 million individual clients are registered on the Moscow Exchange (representing nearly half the economically active population), holding assets totaling more than 11 trillion RUB. Legal entities, meanwhile, have portfolios exceeding 15 trillion RUB. Despite a recent minor decline, the market capitalization (around 23% of GDP) indicates substantial room for growth.

The President proposed three specific initiatives to boost capitalization and investor confidence:

Stimulating Equity Placement (IPO Program): While bonds and collective funds are growing, debt alone cannot fuel long-term development; equity capital (like an IPO) is essential. To incentivize this, the government is tasked with forming a program for the primary and secondary placement of shares of state-participated companies. Furthermore, the Ministry of Economic Development is asked to draft sectoral plans for listing major issuers and link existing support measures to a company’s public status. For example, a borrower from the Industrial Development Fund could receive a lower loan rate if they conduct an IPO. This is like offering a significant discount to a private company when it decides to “go public” and share ownership broadly, rewarding transparency and market participation.

Enhancing Transparency and Value Creation: To build investor trust, the President requested that the government ensure the largest state-participated companies join the “Shareholder Value Creation Program” by the end of the following year. This initiative, developed by the Central Bank, Moscow Exchange, and Ministry of Finance, is based on similar successful experiences in Asian countries. It requires participating companies to publish key metrics—such as net assets, dividend yield, and development forecasts—that are crucial for investor decision-making. Additionally, the performance incentives for executives in these companies should be directly tied to increasing shareholder value.

Expanding Family Savings Incentives: Building on the existing program for long-term savings (which already includes over 8 million contracts totaling nearly 560 billion RUB), the President focused on encouraging “family savings”. Parents who open long-term savings products for their children can now receive a personal income tax (NDFL) deduction. The size of this deduction is calculated based on the actual contribution, up to 500,000 RUB per parent, allowing a maximum deduction sum of 1 million RUB per family. Furthermore, tax benefits for employers who co-finance their employees’ long-term savings will take effect in September of the following year.

The New Global Axis: Partnerships, Digitalization, and Energy

The forum heavily underscored Russia’s focus on non-European partners. President Putin confirmed the intent to elevate cooperation with the People’s Republic of China and the Republic of India to a qualitatively new level, with a strong focus on the technological component. This involves joint projects spanning energy, industry, space, and agriculture.

This strategic pivot is not merely about trade volume; it is rooted in technological competence and infrastructure development. Maxim Oreshkin highlighted that Russia, China, and India possess serious competencies in digital solutions, enabling their companies to actively compete and expand globally. Russian firms, particularly those dealing in platform solutions (like urban services and trading marketplaces), are expanding successfully across the globe.

A unique element of Russia’s technological partnership approach is its commitment to digital sovereignty. When Russian solutions are introduced in third countries, the objective is not simply to compel users onto a single platform. Instead, Russia expresses a readiness to transfer these solutions to help partner nations establish their own digital sovereignty, recognizing that sovereign partners are the most reliable in the long term.

The future of Russia’s collaboration with Asia is dramatically illustrated in the energy sector, which is undergoing a global transformation driven by the accelerating demand from computational power and Artificial Intelligence (AI). Minister Reshetnikov detailed plans to introduce 155 GW of new generating capacity by 2045, with 17 GW of new capacity and 21 GW of modernization planned by 2030. This massive modernization program is financed through mechanisms like capacity connection agreements.

A particularly forward-looking idea for Russian-Chinese cooperation involves moving away from exporting raw energy resources. Instead, highly prospective projects center on building isolated generation and computing power near the source of primary energy. This means that instead of transporting coal or gas vast distances to power centers (like the example of Kuzbass coal being shipped through the Far East to China for a computing center), the final product exported will be computational power itself. This approach minimizes logistics and maximizes efficiency.

Furthermore, critical infrastructure projects like the Northern Sea Route (NSR)—a trans-Arctic corridor stretching from St. Petersburg to Vladivostok—are considered national priorities. This project, which integrates logistics, the development of Arctic cities, and economic projects along its path, has captured international interest and is viewed as a route that will seriously alter global trade flows.

A Vision for Integrated Growth

The VTB Investment Forum provided a clear articulation of Russia’s economic strategy: successfully managing external challenges by emphasizing market flexibility, financial stability, and internal resource mobilization. President Putin’s address cemented the agenda for the immediate future, mandating the expansion of the capital market through structural reforms and targeted incentives. By coupling these reforms with deep, strategic partnerships with countries across Asia, the Middle East, and Africa, particularly in cutting-edge fields like digital technology and integrated energy solutions, Russia aims to achieve not just resilience, but a self-sustaining model of long-term, sovereign economic growth. The path forward is defined by strengthening internal financial mechanisms and creating technological and logistical bridges to a rapidly transforming multipolar world.

Join the Conversation:

📌 Subscribe to Think BRICS for weekly geopolitical video analysis beyond Western narratives

Outstanding analysis of how economic sovereignty emerges through coordinated fiscal adaptation. Your point about the ruble trade shift from 14% to 57% captures somethingcrucial: the metric isn't just substitution, it's the downstream compounding effects on domestic capital formation and pricing power.

What's understated here is the timeline friction. Even with a functional capital market architecture, the liquidity premiums for ruble-denominated debt versus cross-border alternatives will distort allocation for atleast a decade. The IPO pipeline sounds compelling, but if institutional buyers are largely state-adjacent, you're back to crowding out efficiency signals.

Impressive!